Macro and Manufacturing Pulse: Navigating the Crossroads of Tariffs, Technology, and Transformation

Date: June 21 - June 27, 2025 Prepared For: SME Manufacturing CEOs & Leadership Teams By: James Danowski, PhD, President and Senior Data Scientist, IntelliSell

Executive Summary

Welcome, SME Leaders and interested others, to this edition of the weekly manufacturing intelligence reports.

The U.S. manufacturing sector is undergoing a profound strategic realignment. Evolving trade policies require rapid adjustments, but forward-looking SME leaders are turning short-term shifts into a historic opportunity to strengthen American production and technological leadership. Recent trends in the automotive, electronics, and agricultural sectors show how short-term supply chain maneuvers now coexist with bold, long-term bets on a resilient, reshored future. Companies are mastering this ‘tariff tap dance’ by balancing tactical moves with billions in new domestic investments, creating a complex yet purposeful period of industrial transformation.

Conflicting signals and persistent ambiguity mark today’s operating environment. Key macro indicators diverge: the S&P Global Manufacturing PMI points to expansion, while the ISM PMI shows contraction (S&P Global, YCharts). This gap suggests that recent momentum is fueled more by defensive inventory building ahead of tariff-driven price increases than by true organic demand growth. These trends expose the fragility of legacy offshore models and reinforce the need for resilient, U.S.-based supply chains. While tariffs can increase input costs, they also serve as a vital tool to protect American industry from unfair global competition.

This uncertainty is amplified by weakening industrial production figures and signs of a cooling labor market in manufacturing. Meanwhile, operational headwinds — including a surge in automotive recalls — underscore the systemic risks that come with managing ever-greater product complexity and stretched supply chains (Federal Reserve).

This report offers actionable insights for manufacturing leadership by connecting these high-level macro trends to their direct operational and financial impacts on the automotive, electronics, and agricultural sectors. By presenting quantifiable examples, "So What?" takeaways for executives, and case studies of company adaptations, this brief is designed to equip you with the strategic intelligence needed to navigate the challenges and capitalize on the opportunities of this transformative era.

Strategic Focus Areas

Mitigate Tariff & Geopolitical Volatility: The unpredictable nature of trade policy is the new constant. Action: Develop dynamic, multi-scenario supply chain models to quantify the impact of potential tariff changes and geopolitical disruptions on input costs and profitability.

Harness AI for Competitive Advantage: Artificial intelligence is no longer a future concept but a present-day driver of efficiency and innovation, fueling a supercycle in electronics and transforming operations in all sectors. Action: Move beyond exploration to implementation by identifying high-ROI pilot projects for AI in predictive maintenance, quality control, and supply chain optimization.

Strengthen Supply Chain Resilience: The focus of supply chain management has irrevocably shifted from pure cost optimization to risk mitigation and resilience. Action: Accelerate reshoring and nearshoring initiatives for critical components, diversify the supplier base to reduce single-source dependencies (especially for materials such as rare earth magnets), and invest in digital twin technology to enhance network visibility.

Navigate Sector-Specific Headwinds: Each vertical faces unique challenges, from the EV market's pivot to affordability in automotive to the investment paradox in agriculture. Action: Critically reassess product roadmaps and capital allocation to align with new market realities, such as developing lower-cost models or leveraging cyclical downturns for strategic modernization.

Main Body: Key Macro Trends and Sector-Specific Impacts

Theme 1: The Tariff Effect: Reshaping Supply Chains and Driving Reshoring

The aggressive and unpredictable use of tariffs has become the single most dominant force shaping industrial strategy, acting as both a source of immediate financial pain and the primary catalyst for a long-term transformation of American supply chains.

High-Level Data:

Sportswear giant Nike warned that tariffs could create a $1 billion impact on its earnings ( Manufacturing.net).

Spice manufacturer McCormick cautioned that tariffs could cost the company $90 million annually for ingredients that cannot be grown in the U.S. (Food Dive).

In response to trade pressures, GE Appliances announced a $490 million investment to relocate washing machine production from China to Kentucky, creating 800 new jobs (Manufacturing.net).

The U.S. and China reportedly agreed on a new trade framework to reduce some tariffs and expedite shipments of critical rare-earth magnets. However, details remain opaque, and high tariffs on many goods are still set to be enforced ( FreightWaves, Automotive Logistics).

Profit/Loss Implications:

Tariffs function as a protective measure to level the playing field, but companies must manage the cost pressures they create. In the long term, the sustained risk and cost are fundamentally altering the economic calculus, making the higher fixed costs of domestic manufacturing a justifiable "insurance premium" against global chaos.

"So What?" for Manufacturing Executives:

The primary driver of supply chain strategy is shifting from cost optimization to risk mitigation. Executives must now prioritize network resilience, flexibility, and visibility, as the cost of a line-down situation caused by a sudden trade policy change far outweighs the savings from a globally extended supply chain.

Specific Sector Impacts:

Automotive: The auto supply chain is at the epicenter of the tariff war. Parts suppliers have reported revenue drops of up to 40%, forcing layoffs as automakers delay new model investments ( TT News). Toyota warned tariffs could cost it $1.3 billion (CBS News). The most acute vulnerability is the supply of rare earth magnets from China, which are critical for EV motors and have been restricted since April, remaining a significant geopolitical risk ( IndustryWeek, Entrepreneur).

Electronics: While less exposed to direct tariffs on finished goods, the sector is profoundly impacted by the geopolitical tensions driving trade policy. The entire push for domestic semiconductor production, fueled by the CHIPS Act, is a direct response to the strategic vulnerability of relying on overseas fabs, particularly in Taiwan ( Semiconductors).

Agriculture: While facing broader trade headwinds, such as a record agricultural trade deficit (Agriculture.com, AgWeb), the sector's manufacturing base is a key participant in the reshoring boom, driven by a desire to de-risk supply chains from global volatility (AgWeb).

Quantifiable Impact Example:

A sudden 25% tariff on a critical imported component, such as an automotive ECU or a specialized electronic capacitor, could wipe out the entire profit margin on a finished product if pre-vetted alternative domestic or near-shore suppliers are not available, potentially leading to losses on every unit sold.

Actionable Insights & Strategies:

Accelerate Supplier Diversification: Actively identify and qualify alternative suppliers in different geopolitical regions, with a strong focus on nearshoring opportunities in Mexico, which is increasingly seen as a reliable alternative to Asia (Supply Chain Brain).

Invest in Tariff Modeling: Utilize AI-powered scenario planning tools to model the financial impact of various potential tariff scenarios, enabling more agile and data-driven responses to policy shifts (Supply Chain Digital).

Embrace Design for Resilience: Redesign products to use more standardized, readily available components, reducing dependence on single-source, specialized parts. VW's Scout brand, for example, is rethinking EV motor designs to cut its reliance on rare earths (Supply Chain Brain).

Company Spotlight: GE Appliances

GE Appliances' recent announcement of a $490 million investment to onshore its washing machine production is a landmark example of the reshoring trend in action. The move will shift manufacturing from China to the company's massive Appliance Park headquarters in Louisville, Kentucky, and is expected to create approximately 800 new American jobs. This decision is not being made in a vacuum; it is a direct strategic response to years of supply chain disruptions, rising international shipping costs, and the persistent uncertainty surrounding the U.S.-China trade relationship (Manufacturing.net, IndustryWeek).

This investment represents a calculated trade-off. While domestic labor and operating costs are higher, GE is betting that the benefits of a shorter, more predictable, and resilient supply chain will outweigh those costs. By manufacturing closer to its primary market, the company can reduce lead times, improve inventory management, and mitigate the geopolitical risks and tariff volatility that have plagued global manufacturers. For other manufacturing leaders, GE's move serves as a powerful case study in shifting the corporate mindset from chasing the lowest possible unit cost to investing in long-term operational stability and control.

Theme 2: Economic Crosscurrents: Interpreting Contradictory Market Signals

The macroeconomic landscape is clouded by ambiguity, with key indicators painting conflicting pictures of the manufacturing sector's health. This uncertainty is chilling short-term investment and complicating demand forecasting.

High-Level Data:

Diverging PMIs: The S&P Global Flash US Manufacturing PMI held at an expansionary 52.0 in June, a 15-month high. In stark contrast, the ISM Manufacturing PMI registered a contractionary 48.5 for May (S&P Global, Trading Economics, YCharts).

Faltering Production: U.S. industrial production unexpectedly declined by 0.2% in May, missing market expectations, while manufacturing output increased only marginally by 0.1% (Federal Reserve, Trading Economics).

Cooling Labor Market: The manufacturing sector shed a net 8,000 jobs in May, led by a significant loss of 7,300 jobs in the machinery sector, a key indicator of business investment (Industry Select, BLS).

Profit/Loss Implications:

The primary risk is a "bullwhip effect" where defensive, tariff-driven inventory building creates a false sense of demand, leading to overproduction followed by a sharp drop in orders. This uncertainty freezes capital investment, delaying revenue and potentially ceding ground to more decisive competitors.

"So What?" for Manufacturing Executives:

Leadership cannot take headline data at face value. The divergence in PMI reports indicates that the sector's perceived strength is not due to organic growth, but rather to a defensive, fear-driven pull-forward of demand. The underlying health is more fragile, demanding a cautious approach to capital spending and a focus on operational efficiency.

Specific Sector Impacts:

Automotive: The slowdown is palpable. Automakers are delaying investments in new tooling and models, resulting in a potential drop in revenues of up to 40% for equipment suppliers (TT News). This directly reflects the broader chilling effect of economic uncertainty on big-ticket capital projects.

Electronics: This sector is a tale of two markets. The AI-driven data center and semiconductor segments are booming, providing a powerful tailwind that insulates them from some macroeconomic pressures. However, consumer-facing electronics and other non-AI segments are more vulnerable to cautious spending and rising component costs (PCMag).

Agriculture: This sector is experiencing the contradiction most acutely. Sales of new high-value equipment are plummeting, with 4WD tractor sales down 39.3% and combine sales down 20.9% year-over-year in May (Equipment Finance News). This is a direct result of lower farm incomes and high interest rates, forcing farmers to delay major purchases.

Quantifiable Impact Example:

The 39.3% year-over-year drop in 4WD tractor sales demonstrates the high sensitivity of agricultural capital expenditures to farmer income and interest rates. A sustained period of high rates and low commodity prices could suppress demand for high-margin equipment by a multiple of the decline in net farm income, severely impacting manufacturer revenues.

Actionable Insights & Strategies:

Prioritize Cash Flow and OpEx: In an uncertain demand environment, conserve capital by focusing on operational expenditures that drive immediate efficiency gains over large, speculative capital projects.

Enhance Customer Support: For equipment manufacturers, offer flexible financing options, robust parts and service support, and used equipment trade-in programs to support customers through the downturn and build loyalty for the next upcycle.

Leverage Downtime for Strategic Upgrades: Use any slowdown in production as an opportunity to implement continuous improvement projects, retrain the workforce, and upgrade production lines with less disruption to operations.

Company Spotlight: John Deere & The Ag Sector's Investment Paradox

The agricultural equipment sector provides a fascinating case study in long-term strategic thinking amidst a sharp cyclical downturn. While current sales figures are bleak, the industry's largest players are making massive, counter-cyclical investments in their U.S. manufacturing base. John Deere is leading this charge, announcing a monumental $20 billion, 10-year investment plan for its U.S. production facilities, with $100 million being deployed this year alone on projects in Missouri, North Carolina, Tennessee, and Iowa ( AgWeb).

This is not a contradiction but a sign of profound strategic foresight. Deere, along with competitors like AGCO and CNH Industrial, who are also expanding their U.S. footprints, understands that the current slump is temporary. They are leveraging the period of lower operational tempo to execute a once-in-a-generation overhaul of their production and supply chain infrastructure. By investing now, they can retool factories, integrate new technologies, and strengthen domestic supplier relationships with minimal disruption.

The lesson for other manufacturing leaders is powerful: cyclical downturns can be the ideal time to make foundational strategic investments. While competitors may be pulling back and conserving cash, those with a strong balance sheet and a clear long-term vision can use this time to build a more resilient, technologically advanced, and domestically anchored production base, ensuring they emerge from the downturn with a significant competitive advantage.

Theme 3: The AI Supercycle: Driving a Great Bifurcation in Electronics and Beyond

The explosive demand for Artificial Intelligence is triggering a supercycle in the semiconductor industry, forcing a strategic reconfiguration across the entire electronics sector and sending technological ripples into every corner of manufacturing.

High-Level Data:

Global semiconductor foundry revenue rose 12% year-over-year in Q1 2025 to $72 billion, with AI cited as the centerpiece of growth (Semien Engineering).

Global capacity for advanced chipmaking (7nm and below) is forecast to grow by 69% between 2024 and 2028, driven by demand for AI applications (Semien Engineering, Semiconductor Digest).

Texas Instruments announced plans to invest over $60 billion to build new semiconductor fabs in the U.S. (Manufacturing Dive, Semiconductor Digest).

McKinsey anticipates AI could boost R&D throughput for semiconductors by almost 60% (Semien Engineering).

Profit/Loss Implications:

The AI boom is creating immense wealth for a concentrated group of companies at the core of the hardware ecosystem (e.g., Nvidia, TSMC, Broadcom), whose valuations have soared (Tipranks). Conversely, it's forcing other companies to incur significant restructuring costs as they shed non-core assets to focus their capital on the AI race.

"So What?" for Manufacturing Executives:

AI is a foundational technology that is forcing strategic divergence. Companies must make a critical choice: either commit the massive capital required to compete at the leading edge of foundational AI hardware or pivot to a specialized strategy, designing niche applications or integrating AI into existing products in a unique way.

Specific Sector Impacts:

Automotive: While not a direct player in the chip-making boom, the auto industry is a critical consumer. The push toward software-defined vehicles makes access to advanced, AI-capable chips a strategic necessity. The industry's complexity is also a target for AI-driven design and manufacturing optimization tools ( IndustryWeek).

Electronics: This is the heart of the bifurcation. Intel announced it is shutting down its automotive business unit to focus capital on its core foundry and data center CPU businesses (Manufacturing Dive, Semien Engineering) In a complementary move, auto supplier Continental is establishing a fabless semiconductor organization, focusing on chip design while outsourcing the capital-intensive manufacturing (Manufacturing Dive, Semein Engineering).

Agriculture: AI is the engine of the next wave of precision agriculture. It is being used in smart drones to monitor crop health (Precision Farming Dealer), and major players, such as Deere, are acquiring AI-related startups to bolster their autonomous and precision capabilities (Manufacturing Dive).

Quantifiable Impact Example:

Siemens' new AI-enhanced Electronic Design Automation (EDA) toolset allows chip designers to create custom AI workflows (Semien Engineering). For a complex chip design that typically takes 18-24 months, leveraging such a tool to accelerate verification and validation could shorten the time-to-market by 3-4 months, representing tens of millions of dollars in potential revenue and a significant competitive edge.

Actionable Insights & Strategies:

Define Your AI Strategy: Determine whether your company will be a producer of foundational AI technology, a specialist designer of AI-powered components, or a consumer integrating AI to enhance products and operations.

Invest in an AI-Ready Workforce: The most desired skill in the European semiconductor industry is now AI/machine learning (Semien Engineering). Invest in upskilling and retraining programs to build internal AI talent.

Modernize the Tech Stack: Adopt digital design platforms that enable greater collaboration among engineering, supply chain, and manufacturing teams, as exemplified by Northrop Grumman's utilization of digital twins and XR environments (IndustryWeek).

Company Spotlight: The Intel / Continental Divergence

The strategic moves announced by Intel and Continental this past week perfectly illustrate the "great bifurcation" being driven by the AI supercycle. Intel, a titan of the semiconductor industry, announced it is shutting down its automotive business unit. This is not a sign of failure, but a calculated strategic decision to shed a non-core asset and focus its immense capital resources on the primary battle: building next-generation fabs to compete with TSMC in the high-stakes foundry business and producing high-performance CPUs for the AI data center boom (Manufacturing Dive, Semien Engineering).

Simultaneously, Continental, a major automotive supplier, announced it is establishing a fabless Advanced Electronics & Semiconductor Solutions (AESS) organization. Continental recognizes it cannot compete with the billions required for fabrication. Instead, it is doubling down on its core competency: designing and verifying specialized chips for automotive applications. It will outsource the actual manufacturing to foundry partners, such as GlobalFoundries. This symbiotic divergence showcases the new industrial structure: a few giants, such as Intel, will build the capital-intensive "engine" of AI, while a host of specialized companies, like Continental, will design the custom parts that plug into that engine. This model allows each company to focus its resources where it has the greatest competitive advantage.

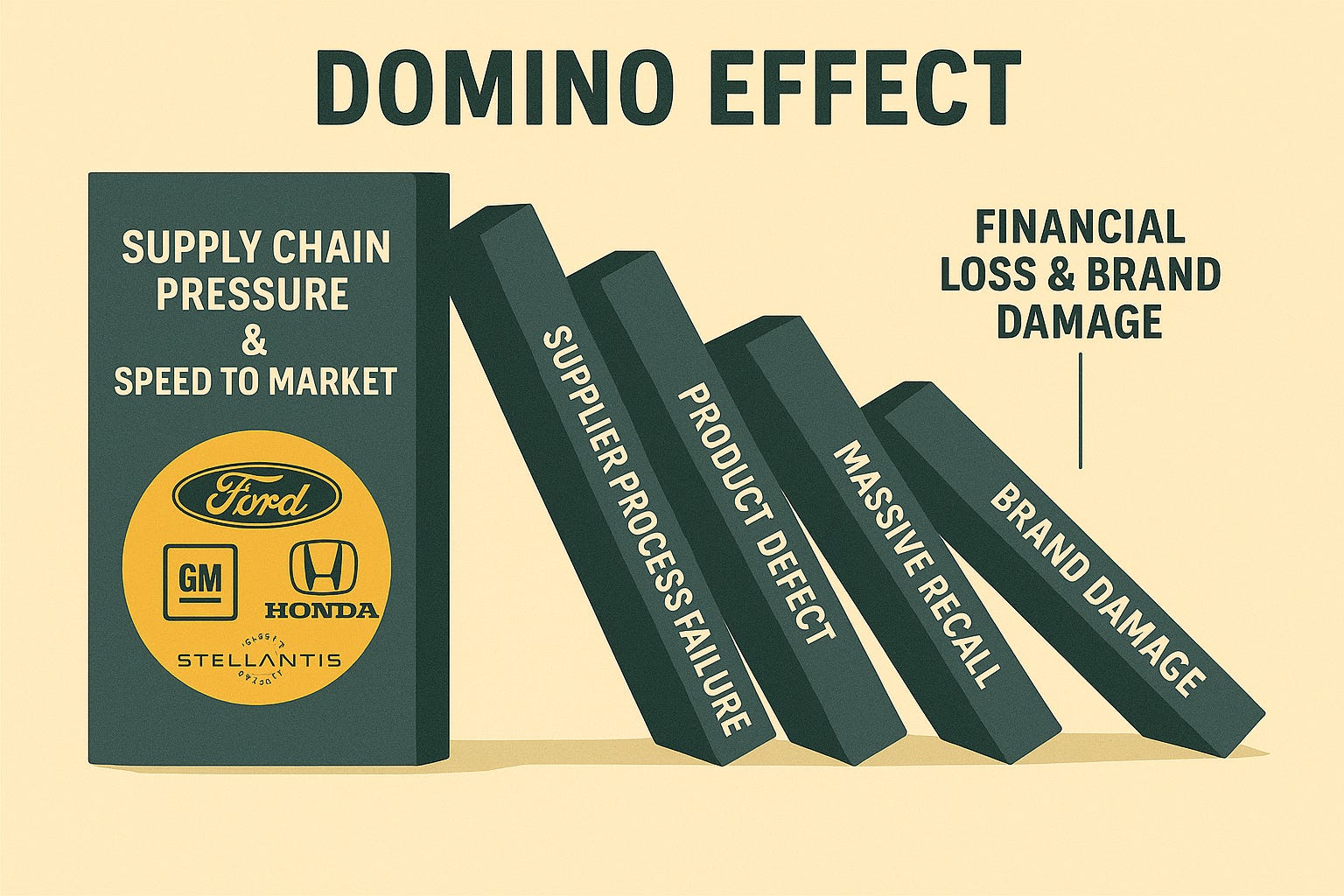

Theme 4: Operational Headwinds: Managing Complexity, Quality, and Recalls

A surge in large-scale product recalls, particularly in the automotive sector, highlights a growing systemic challenge for manufacturers: managing the immense complexity of modern products and supply chains in a high-pressure environment.

High-Level Data:

Ford Motor Company: Recalled over 300,000 Explorer and Aviator SUVs for seat switch issues and ordered a "stop sale" for its electric Mustang Mach-E due to a software flaw that could trap drivers (Automotive Dive, Manufacturing.net).

General Motors: Recalled over 41,000 Cadillac Lyriq EVs for blank instrument displays and 62,000 Chevrolet Silverado trucks for a fire risk from a brake system short (Automotive Dive).

Honda: Recalled 259,000 vehicles for a brake pedal defect explicitly attributed to "insufficient training at a supplier," resulting in improperly assembled components (Automotive Dive).

Stellantis: Recalled over 330,000 Jeep Grand Cherokee SUVs due to a steering wheel issue that could cause a loss of control (Click on Detroit).

Profit/Loss Implications:

The direct costs of recalls—including parts, labor, logistics, and potential regulatory fines—can run into hundreds of millions of dollars. The indirect costs are often greater, manifesting as significant brand damage, loss of consumer trust, diminished resale values, and a negative impact on stock performance.

"So What?" for Manufacturing Executives:

The wave of recalls is a critical symptom of deeper issues. The rapid transition to complex, software-defined products has exponentially increased potential points of failure, while strained supply chains and pressure to accelerate development are impacting quality control. Quality can no longer be a final-stage inspection; it must be a core principle integrated throughout the entire value chain, from initial design to supplier management and final assembly.

Specific Sector Impacts:

Automotive: This sector is the clear epicenter. The recalls demonstrate systemic challenges with both hardware and software. The issues with the Mustang Mach-E and Cadillac Lyriq are direct consequences of software complexity. At the same time, the Honda recall is a stark example of a supplier process failure having massive downstream implications.

Electronics: While not facing vehicle-style recalls, the pressure of the AI race creates immense risk for costly bugs and chip yield issues. Robust design verification and validation are paramount. The development of advanced EDA tools by companies like Siemens is a direct response to managing this complexity (Semien Engineering).

Agriculture: This sector faces a distinct operational headwind in the form of the "right-to-repair" lawsuit. A federal court denied John Deere's motion to dismiss the FTC's lawsuit, which alleges that Deere has illegally restricted farmers' ability to repair their equipment (DTNNFP, Manufacturing Dive). A loss in court could fundamentally disrupt the highly profitable parts and service business model for all major equipment manufacturers.

Quantifiable Impact Example:

For an SME parts supplier, being identified as the root cause of a major OEM recall, as in the Honda case, is an existential threat. The direct liability for the cost of the recall could be crippling, and the reputational damage could lead to the termination of major contracts, effectively putting the company out of business.

Actionable Insights & Strategies:

Embed Quality into Design (DfQ): Utilize digital twin technology and advanced simulation tools to stress-test designs for potential physical and software failures before a single part is manufactured (IndustryWeek).

Mandate Deeper Supplier Transparency: Move beyond simple quality audits. Implement shared, real-time quality monitoring platforms with Tier 1 suppliers and demand greater visibility into their own process controls and training protocols.

Isolate and Invest in Software Validation: Treat vehicle and product software as a critical component with its dedicated quality assurance lifecycle. Invest in automated testing, over-the-air (OTA) update capabilities, and "red team" cybersecurity testing to identify flaws before they reach the customer.

Company Spotlight: Honda's Supplier-Driven Recall

Honda's recent recall of 259,000 vehicles provides a powerful and cautionary tale for the entire manufacturing industry. The issue was a potentially faulty brake pedal, but what made this recall particularly noteworthy was the company's explicit and public attribution of the cause: "insufficient training at a supplier" led to improperly assembled components (Automotive Dive). This is a rare and telling admission that moves beyond the typical explanation of a simple defective part.

This incident highlights the significant vulnerability that manufacturers face within their supply chains. It demonstrates that a failure in a partner's human processes—in this case, training—can have a direct, massive, and costly impact on the OEM's final product and brand reputation. In an environment where supply chains are still recovering from disruptions and the pressure to control costs is intense, the risk of such quality lapses from external partners is magnified. For manufacturing CEOs, the Honda case is a stark reminder that their quality management systems cannot end at their factory gates. It underscores the critical need for deeper integration, more rigorous process verification, and truly collaborative partnerships with suppliers to ensure that every component, as well as the processes behind it, meet the required standards.

Conclusion & Key Executive Takeaways

The U.S. manufacturing sector is in a state of controlled chaos, characterized by a strategic pivot away from the old paradigms of globalization and cost optimization toward a new era that prioritizes resilience, technology, and domestic capability. The primary challenge for leadership is managing the acute short-term pain of tariff-driven cost pressures and economic uncertainty while maintaining the long-term vision and investment required to thrive in this new landscape. The increasing complexity of modern products adds another layer of risk, demanding an unprecedented focus on quality control.

To succeed, executives must re-emphasize a set of core actionable pillars:

Embrace Proactive De-risking: Treat supply chain resilience not as a cost, but as a competitive advantage. The time for reactive adjustments is over; proactive investment in diversification and domestic capacity is now essential.

Commit to an AI-Driven Future: Integrate AI strategically into both products and processes. The companies that win the next decade will be those that successfully leverage AI to design better products, run more efficient factories, and build more intelligent supply chains.

Lead Through Ambiguity: In a market of conflicting signals, clarity of vision is paramount. Use cyclical downturns as opportunities for strategic modernization and communicate a steady, long-term plan to stakeholders, customers, and employees.

Champion End-to-End Quality: As products become more complex, quality cannot be an afterthought. It must be a foundational principle embedded in design, sourced from trusted partners, and verified continuously through production.

The path ahead is complex and volatile, but for leaders who navigate these crosscurrents skillfully, the opportunity to build a stronger, more competitive, and more resilient American manufacturing base is immense. This pivotal moment is a chance to secure America’s industrial future on its own terms — strong, self-reliant, and built to last.

Stay strong, agile, and resilient!

James Danowski, PhD, IntelliSell